Buy and Borrow

Credit Card Balance Transfers: What You Need to Know (Video)

January 24, 2018

High interest rate credit cards get expensive quick. The costs from those interest rates each month can make it harder to get out of debt.

Credit card balance transfers are a way to get out of that high interest rate debt cycle. Let’s go through what a balance transfer is, how it works and why you might want to consider using one.

What is a Balance Transfer?

A balance transfer is when you transfer the debt from one credit card to another credit card. So if you have a credit card with a high interest rate, you can transfer the balance from that card to a credit card with a lower interest rate.

How Do Balance Transfers Work?

Let’s say you have two credit cards. One has a higher interest rate than the other. You can go to the lender of the card with the lower interest rate and request to transfer the balance from the higher interest rate card over to the lower interest rate card.

If you only have one credit card with a high interest rate, you can still potentially take advantage of balance transfer offers from lower rate credit cards. You would apply for the new, lower interest rate credit card first, then follow the steps to transfer your balance upon approval.

Even if you have multiple high rate credit cards, balance transfers can still work. You can often transfer more than one balance to the lower interest rate card as long as the total amount of the balance transfer doesn’t exceed your available credit limit.

How Can I Benefit From a Balance Transfer?

Saving money is the biggest benefit of credit card balance transfers. The higher your interest rates are, the more you will pay over time. So you can see major long-term savings when you transfer a balance to a lower interest rate card.

Another benefit is to simplify your credit card payments. If you have several high interest rate cards with different due dates and payments, it can be tricky to manage. Transferring the balances onto one low interest rate card can help consolidate debt and make it easier to manage.

What Should I Look for in a Balance Transfer?

Balance transfers can make your life easier and save you money. But it’s important to note that some balance transfer offers are better than others.

Always read the fine print.

Like any contract, read the fine print before you do a balance transfer. Make sure that you know about all the fees associated with the new card. See if there is a time limit attached to the interest rate. Look for any hidden costs that might be associated with the offer.

Make sure the interest rate isn’t a short-term offer.

Some balance transfers offer a low interest rate for a short period of time, like six months to a year. After that, the interest rate can increase, sometimes to a higher rate than you had in the first place.

Unless you can pay off the whole balance during this time period, these offers might not save you money. Instead, look for a balance transfer that lets you keep the interest rate until your balance is paid in full.

Factor in the cost of fees before deciding on a balance transfer.

Again, balance transfers are meant to save you money over time. But some offers include large transfer fees just to move your balance to the new card.

You also should consider the other credit card fees associated with a card before you transfer your balance to it. If the lower interest rate card charges a transfer fee and includes an annual fee, make sure that you’ll still save money after paying all of that.

Ideally, try to find a credit card that offers no annual fee and no transfer fee to make sure that you get the savings you need from the balance transfer.

Category

Buy and Borrow

Tags

Business

What’s Needed for a Business Loan?

Before you apply for a business loan, learn about the eligibility requirements and what is needed to qualify for a small business loan.

Simply Suncoast

Credit Union Near Me… No Matter Where I Am

When you are looking for a credit union nearby, there is something wonderful you should know. Even if your credit union is not in the area, you can likely access credit union services.

Safety and Protection

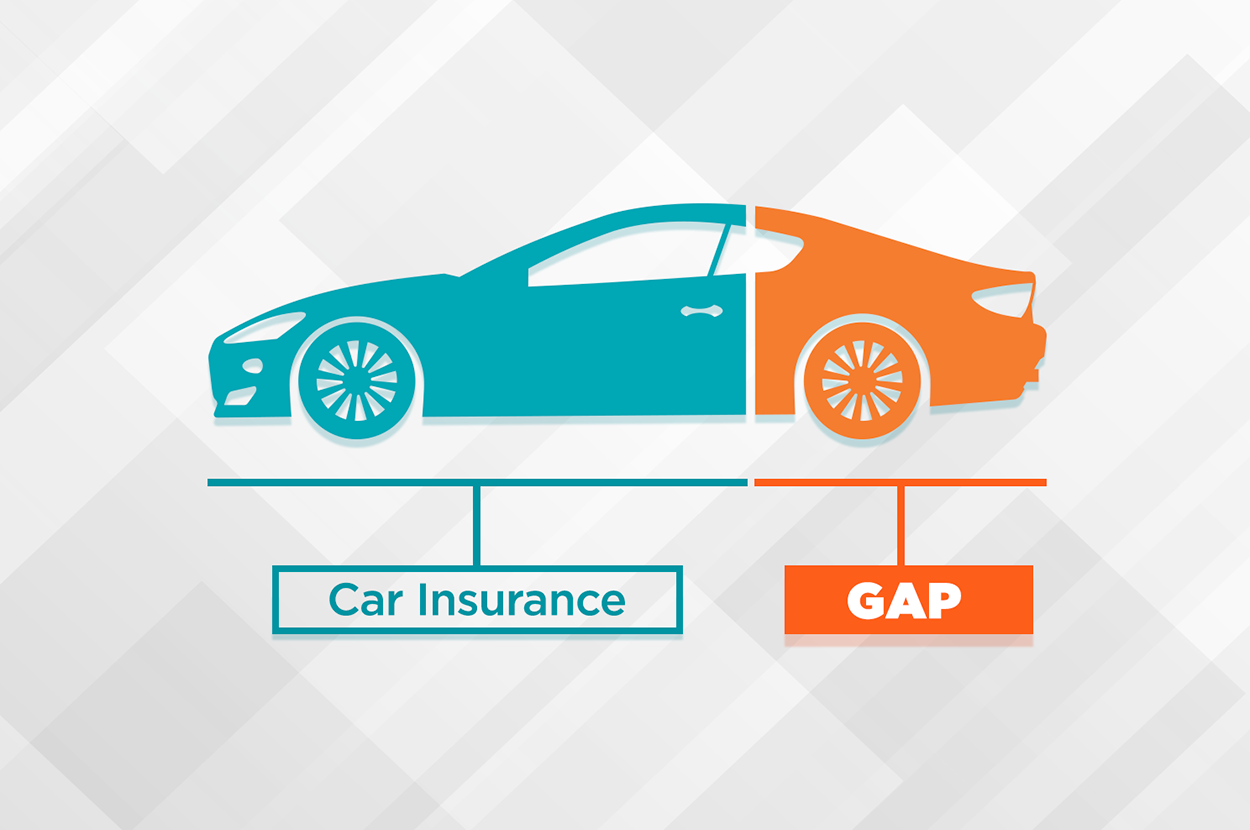

What Is GAP and What Does it Cover?

If you’re making car payments, Guaranteed Asset Protection (GAP) is a type of coverage that can save you a ton of money if your car is lost or totaled. Let’s explore what GAP is and what it covers.